March days’ supply of vehicle inventory ranked by auto brand.

As the automotive industry navigates the effects of new tariffs, the supply of new vehicles on dealer lots across the U.S. has fallen, according to the Cox Automotive analysis of vAuto Live Market View data released on April 10.

New-vehicle inventory levels at the start of April decreased from March and were lower than in early April 2024. New vehicle sales surged in March, driven by strong seasonal trends and the urgency created by the import tariff announcement.

As April opened, the total supply of new vehicles on dealer lots across the U.S. was at 2.69 million units, down 10.2% from the 2.99 million units at the start of March and down 2.4% from a year ago.

New vehicle sales increased monthly and yearly in March. The 30-day weekly sales pace in the final measure of March was up 17.2% compared to late February and up 11.9% compared to the same period last year.

Retail vehicle sales have shown strong seasonal trends so far this year. The new retail sales pace increased almost every week in February and March, with a strong surge at month-end with the import tariff announcement creating urgency in the final five days of the month.

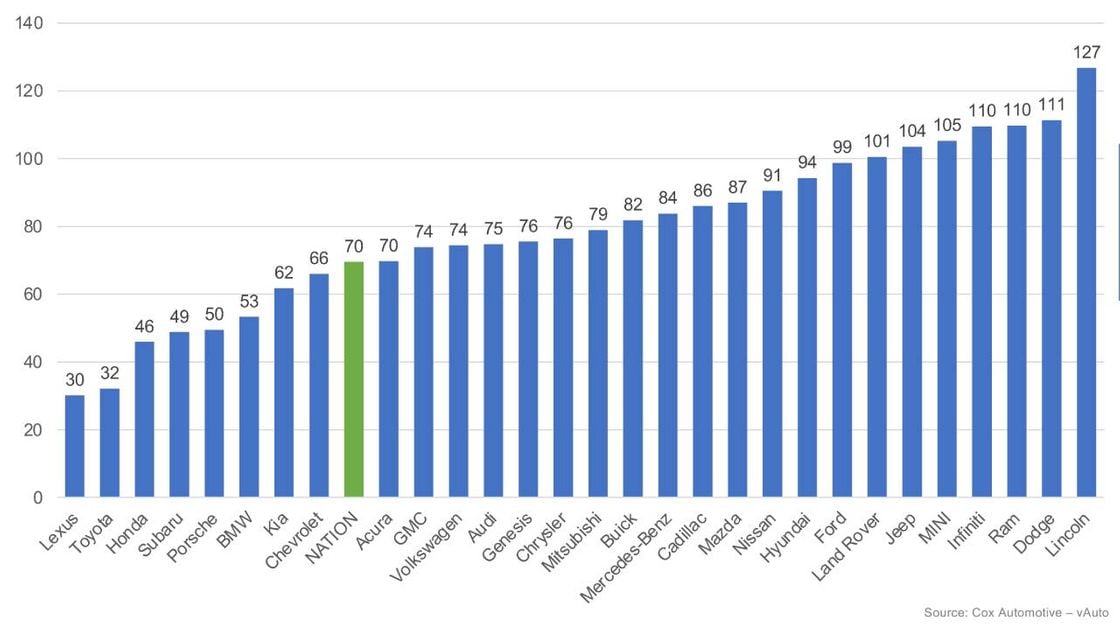

The Cox Automotive days’ supply is based on the estimated daily retail sales rate for the most recent 30-day period. The new vehicle days’ supply was 70 at the start of April, down 21 days from the upwardly revised 91 days at the beginning of March. To start April, days’ supply was down 10 days compared to last year, returning inventory to levels last seen in 2023.

New-vehicle inventory had been relatively stable until the end of March when the sales surge reduced inventory and days’ supply tightened even more. Among the mainstream automakers tracked, 10 have seen their days’ supply decrease by 30 days or more month over month, with Lincoln dropping the most with a 54-day decrease. With import tariffs now in place and parts tariffs likely to start in May, Cox expects supply to tighten even more in the weeks ahead.

New-Vehicle Pricing Declines in March

The average new vehicle listing price was $47,962, down 0.6% from the revised $48,272 at the start of March but higher by 1.9% from a year earlier. At the beginning of April, among the five top-selling automakers, Ford’s average listing price experienced the largest drop of $599, followed by Hyundai with a decrease of $380, and Chevrolet, which was only $57 lower than the previous month. The average listing prices for Honda and Toyota rose in early April, increasing by $212 and $187, respectively.

As reported earlier, a new vehicle’s average transaction price (ATP) was $47,462 in March, down 0.2% monthly and up 0.3% year over year. In March, new-vehicle sales incentives were 7%, or $3,339, virtually flat month over month.

What to Expect in April and Beyond

Tariffs will spike the costs of imported new vehicles. As pre-tariff inventory is depleted, automakers distribute these additional costs across their entire portfolio of vehicles. Tariffs led to a surge in March sales, reducing inventory levels, especially for manufacturers with already low stock levels.

Due to these tariffs and the tightening inventory, and without a policy change in Washington, consumers should anticipate higher prices and fewer discounts on new vehicles by summer. Over time, vehicle buyers can expect a decline in production and sales, leading to increased prices for new and used cars. Additionally, some models may be discontinued as automakers adjust their strategies to cope with the latest economic landscape.

Starting in Q2, the tighter supply and higher prices will likely mirror the conditions in 2021, when the chip shortage affected global vehicle production. Tariffs will drive higher prices, lower production and supply, and slower vehicle sales, creating a challenging environment for consumers and automakers.

Originally posted on Automotive Fleet