The artificial intelligence (AI) race is in full swing, and advanced semiconductors are critical to handle the vast data needs. You’re probably aware of chipmakers like Taiwan Semiconductor Manufacturing, Advanced Micro Devices, and Intel, but what about chip companies that don’t actually manufacture chips?

Arm Holdings (ARM 1.92%) is such a company, and the stock is on fire, having risen 139% since its IPO and more than 215% over the past year. There is a ton to like about the company, but the stock may be ahead of its skis.

What does Arm Holdings do?

Arm Holdings is a critical cog in the semiconductor industry despite not manufacturing chips. Arm designs the framework, which it calls the architecture, for advanced-performance central processing units (CPUs). Its customers use the designs as a base to customize them for their specific needs. You probably use an Arm-based chip every day since 99% of smartphones rely on an Arm-designed processor. Arm makes money by licensing the architectures and from royalties for each product sold. To date, 280 billion have shipped, according to Arm.

AI is a gigantic market for Arm. For instance, Microsoft‘s Copilot+ PC, which incorporates AI into Microsoft 365, utilizes Arm technology. The company expects 100 billion AI-enabled chips to ship by the end of fiscal 2026.

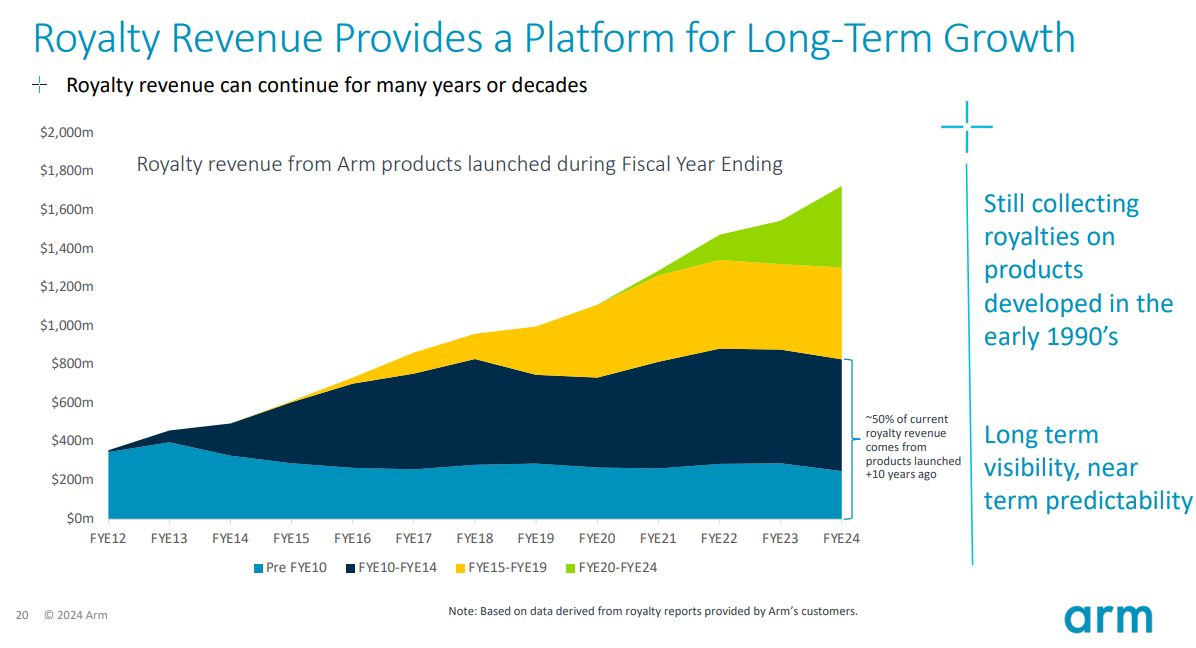

Investors should know two other positive facets of Arm’s business. First, its revenue from legacy products lasts for decades. As shown below, new products stack revenue on top of legacy products rather than cannibalizing it.

Data source: Arm Holdings.

Collecting royalties from products developed long ago is highly profitable because the costs, like research and development, were expensed back when the products were developed.

Finally, Arm’s financial results are similar to those of software companies. As shown below, its gross margin is more comparable to that of software company Palantir than Taiwan Semiconductor, which is also a terrific company.

ARM Gross Profit Margin (Quarterly) data by YCharts

The high gross margin means that Arm will likely be very profitable as it grows. The company also generates healthy free cash flow. Over the past 12 months, Arm reported $709 million in free cash flow on $3.5 billion in sales. This 20% margin means 20 cents of every dollar it earns falls into the company’s pocket.

Arm is clearly a tremendous company, but this doesn’t mean it is a good investment at the current price.

It pays to be patient

Lou Simpson, one of Warren Buffett’s former stock pickers at Berkshire Hathaway, once said, “Even the world’s greatest business is not a good investment if the price is too high.” This seems to be the case with Arm stock.

As shown below, Arm’s valuation towers over industry titan Microsoft and exceeds high-flying AI stock Palantir.

ARM PS Ratio data by YCharts

The downside risk is much higher than the potential upside at over 40 times sales and 160 times operating cash flow. Even when factoring in sales growth, the forward price-to-sales ratio only falls to 37, which is still very high.

Investors who want to own Arm can proceed in a few ways. Dollar-cost averaging over a long period is an excellent strategy to reduce the risk of purchasing at an extravagant price. However, the best strategy may be to keep a close eye on the stock and wait for a significant dip in the share price before buying.

Bradley Guichard has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Berkshire Hathaway, Microsoft, Palantir Technologies, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Intel and recommends the following options: long January 2026 $395 calls on Microsoft, short January 2026 $405 calls on Microsoft, and short November 2024 $24 calls on Intel. The Motley Fool has a disclosure policy.