American stock exchanges currently host eight American technology companies with valuations of $1 trillion or more, but only three have graduated into the $3 trillion club so far:

Apple: $3.7 trillion

Nvidia: $3.3 trillion

Microsoft: $3.3 trillion

Amazon(NASDAQ: AMZN) is the world’s fourth-largest company, at this writing, with a market capitalization of $2.4 trillion. Its stock has soared by more than 50% this year and trades at an all-time high. The company’s strong cloud growth, soaring profits, and leadership position in artificial intelligence (AI) have contributed to the solid gain.

Below, I’m going to explain why Amazon has a legitimate mathematical path to becoming the newest member of the $3 trillion club in 2025.

Amazon is the world’s largest e-commerce company, but it also leads the cloud computing industry through its Amazon Web Services (AWS) platform. It provides businesses with hundreds of services to help them operate in the digital age, from simple data storage to complex software development tools.

However, AWS is also home to many of Amazon’s AI initiatives. Its goal is to dominate the three core layers of AI: Hardware, large language models (LLMs), and software, in order to become a one-stop shop for developers and businesses.

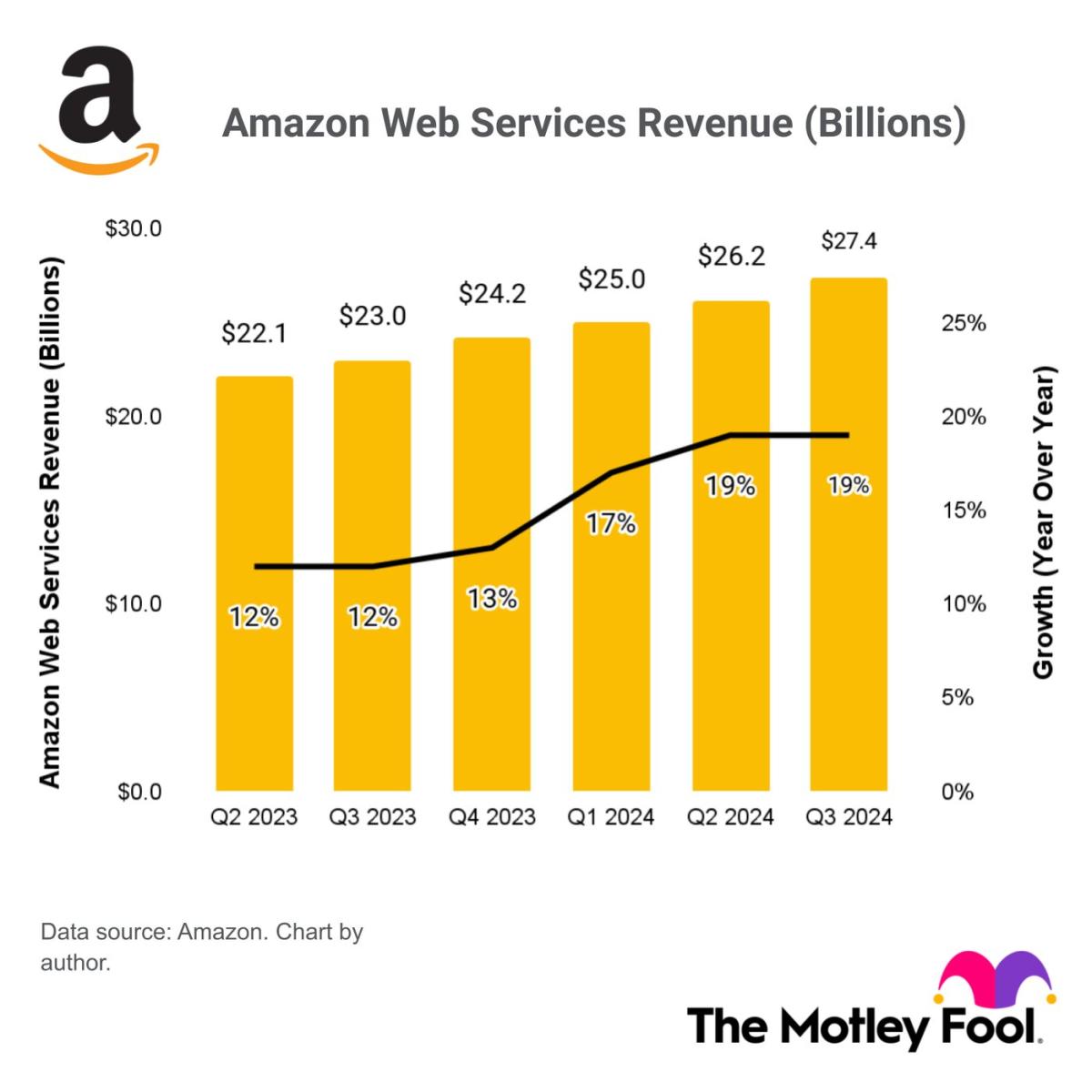

In the third quarter of 2024 (ended Sept. 30), AWS generated a record $27.4 billion in total revenue, which was a 19% increase from the year-ago period. That growth rate has accelerated during 2024, and AI is a big reason why.

Amazon CEO Andy Jassy said the AI business within AWS grew by a triple-digit percentage during Q3 compared to the year-ago period. He also said it’s growing three times faster than the cloud division did at the same stage of its lifecycle.

A chart of Amazon Web Services quarterly revenue and growth rates.

Circling back to the three AI layers, AWS operates data centers filled with Nvidia’s latest AI chips, and it rents the computing capacity to customers for a fee. The company also designed its own chips, which are called Trainium (for AI training) and Inferentia (for AI inference workloads). Amazon says developers can save 50% on training costs by using Trainium1 compared to competing chips, and with Trainium2 now rolling out, those savings could increase even more.

Many developers prefer using ready-made LLMs from third parties rather than building their own because it saves time and money. On the Bedrock platform in AWS, they can access the Titan family of LLMs, which Amazon built in-house. But Bedrock also hosts the latest LLMs from industry-leading companies like Anthropic and Meta Platforms, so customers have no shortage of options. That covers the second layer.

Finally, at the software layer, Amazon developed an AI assistant called “Q,” which can answer questions about an organization’s internal data, or it can be prompted to generate computer code to speed up software projects. Amazon says Q has the highest code acceptance rate in the entire industry, and it even helped the company save 4,500 developer years (and $260 million) on one internal software project alone.

Amazon brings in more than half a trillion dollars in revenue each year across all of its businesses. It isn’t easy to generate growth when the company is already the world’s biggest player in e-commerce and cloud computing, and it’s fast becoming a leader in other segments like streaming and digital advertising. It becomes harder and harder to attract enough new customers to move the needle with each passing year.

However, Amazon is delivering substantial growth at the bottom line by carefully managing expenses and by improving efficiency. The company transformed its e-commerce logistics network last year by slicing the U.S. market into eight regions so that each order travels a shorter distance to reach the customer. So far, the change has yielded a 25% improvement in Amazon’s ability to accurately distribute products across its fulfillment centers.

The company is investing heavily in technology to improve efficiency even further. Its robotics inventions are speeding up the picking, packing, and shipping processes, and AI-powered tools like Project Private Investigator ensure customers don’t receive defective products, which reduces the frequency of refunds and returns. Thanks to all of these improvements, a record number of customers now receive their orders on the same day, and Amazon is steadily shrinking its cost to serve.

Overall, Amazon’s total operating expenses came in at $402.7 billion through the first three quarters of 2024, which was an increase of just 5.6% compared to the same period last year. Meanwhile, the company’s total revenue jumped 11.2% to $450.1 billion.

As a result, Amazon’s net income surged by a whopping 98% to $39.2 billion, which puts the company on track for its highest annual profit ever.

Image source: Amazon.

Amazon’s net income through the first three quarters of 2024 translates into $3.67 in earnings per share (EPS). According to Wall Street’s consensus forecast (provided by Yahoo), the company’s total EPS for 2024 is likely to come in at around $5.14 once the year officially wraps up.

Based on Amazon’s stock price of $227.46 as of this writing, it trades at a price-to-earnings (P/E) ratio of 44.2. That isn’t necessarily cheap because the Nasdaq-100 technology index trades at a P/E ratio of 34.9. But Amazon deserves a premium thanks to its rapid EPS growth, its dominance in industries like e-commerce and cloud computing, and its leadership position in AI.

Now, let’s turn to next year. Wall Street’s consensus forecast suggests Amazon will generate $6.19 in EPS during 2025, placing its stock at a forward P/E of 36.8. That’s almost aligned with where the Nasdaq-100 is now. However, Amazon stock will have to rise 20% next year in order to maintain its current P/E ratio of 44.2.

That alone would take its market capitalization to $2.9 trillion, but here’s where things get interesting. Amazon actually beat Wall Street’s EPS forecast in every quarter of 2024 so far — by an average of 21%. A repeat performance in 2025 would almost certainly send Amazon’s market cap soaring above $3 trillion, assuming a constant P/E ratio.

I think there is a good chance that this will happen, considering Amazon’s focus on efficiency right now, which will remain a tailwind for its earnings. As a result, this company is in a great position to join Nvidia, Apple, and Microsoft in the stock market’s most exclusive club in 2025.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Nvidia:if you invested $1,000 when we doubled down in 2009,you’d have $338,103!*

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $48,005!*

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $495,679!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

See 3 “Double Down” stocks »

*Stock Advisor returns as of December 16, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Apple, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

1 Unstoppable Stock That Could Join Nvidia, Apple, and Microsoft in the $3 Trillion Club in 2025 was originally published by The Motley Fool

Krista Wilson is a news writer for Axe News Room. She has been with the company since 2017. Her favorite topics to write about include local politics and entertainment, but she also enjoys writing about national politics when she can find time between her other assignments.